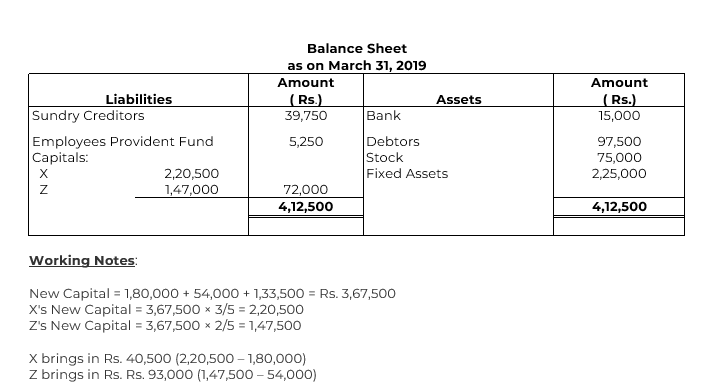

| Liabilities | Amount (Rs.) | Assets | Amount (Rs.) |

| Sundry Creditors | 39,750 | Bank (Minimum Balance) | 15,000 |

| Employees’ Provident Fund | 5,250 | Debtors | 97,500 |

| Workmen Compensation Reserve | 22,500 | Stock | 82,500 |

| Capital A/c : | Fixed Assets | 1,87,500 | |

| X – 1,65,000 | |||

| Y – 84,000 | |||

| Z – 66,000 | 3,15,000 | ||

| 3,82,500 | 3,82,500 |

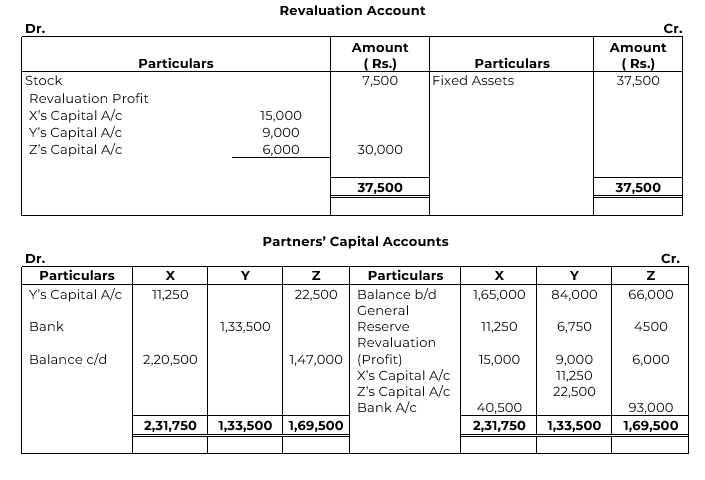

Y retired on 1st April, 2019 and it was agreed that:

(i) Goodwill of the firm is valued at Rs. 1,12,500 and Y’s share of it be adjusted into the accounts of X and Z who are going to share future profits in the ratio of 3 : 2.

(ii) Fixed Assets be appreciated by 20%.

(iii) Stock be reduced to Rs. 75,000.

(iv) Y be paid amount brought in by X and Z so as to make their capitals proportionate to their new profit-sharing ratio.

Prepare Revaluation Account, Capital Accounts of all partners and the Balance Sheet of the New Firm.

SOLUTION