| Liabilities | Amount (Rs.) | Assets | Amount (Rs.) |

| A’s Capital – 1,76,000 | Goodwill | 34,000 | |

| B’s Capital – 2,54,000 | 4,30,000 | Land and Building | 60,000 |

| Workmen Compensation Reserve | 20,000 | Investment (Market value Rs. 45,000) | 50,000 |

| Investments Fluctuation Reserve | 10,000 | Debtors – 1,00,000 | |

| Employee’s Provident Fund | 34,000 | Less: Provision for Doubtful Debts – (10,000) | 90,000 |

| C’s Loan | 3,00,000 | Stock | 3,00,000 |

| Bank Balance | 2,50,000 | ||

| Advertising Suspense A/c | 10,000 | ||

| 7,94,000 | 7,94,000 |

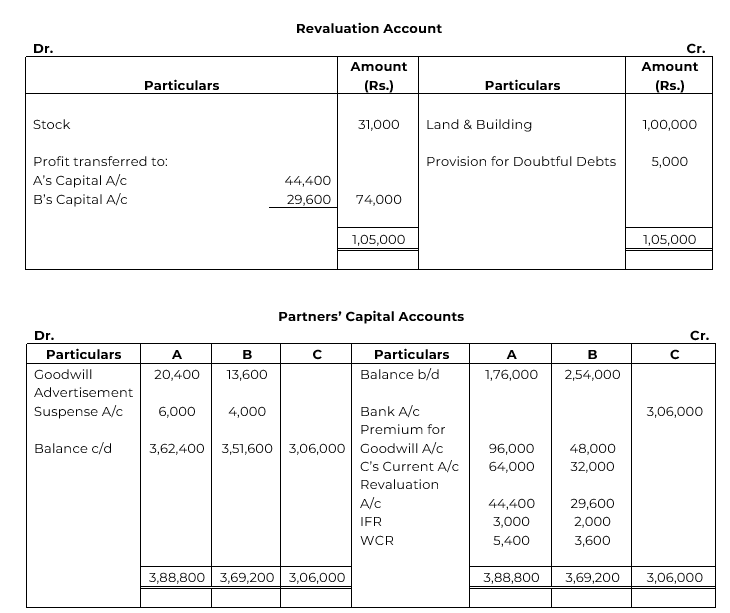

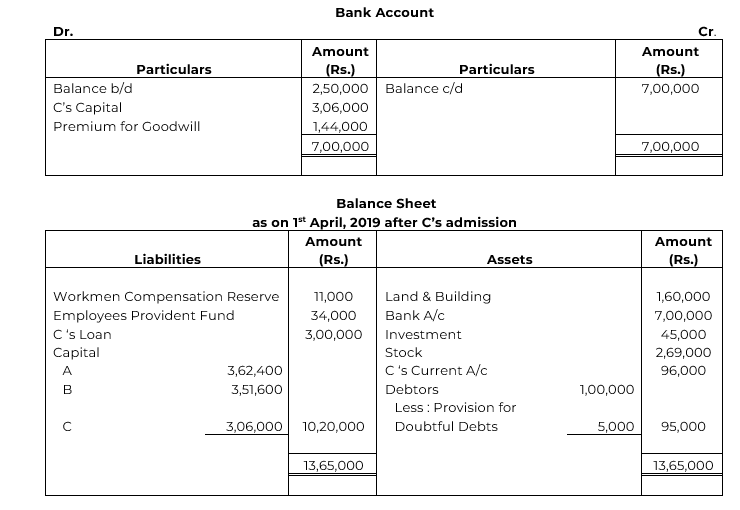

Terms of C’s admission are as follows:

(i) C contributes proportionate capital and 60% of his share of goodwill in cash.

(ii) Goodwill is to be valued at 2 years’ purchase of super profit of last three completed years. Profits for the years ended 31st March were:

2017 − Rs. 4,80,000; 2018 − Rs. 9,30,000; 2019 − Rs. 13,80,000.

The normal profit is Rs. 5,30,000 with same amount of capital invested in similar industry.

(iii) Land and Building was found undervalued by Rs. 1,00,000.

(iv) Stock was found overvalued by Rs. 31,000.

(v) Provision for Doubtful Debts is to be made equal to 5% of the debtors.

(vi) Claim on account of Workmen Compensation is Rs. 11,000.

Prepare Revaluation Account, Partners’ Capital Accounts and Balance Sheet.

SOLUTION