| Liabilities | Amount (Rs.) | Assets | Amount (Rs.) |

| X’s Capital | 52,000 | Goodwill | 8,000 |

| Y’s Capital | 54,000 | Machinery | 38,000 |

| General Reserve | 4,800 | Furniture | 15,000 |

| Sundry Creditors | 5,000 | Sundry Debtors | 33,000 |

| Employees’ Provident Fund | 1,000 | Stock | 7,000 |

| Workmen Compensation Reserve | 10,000 | Bank | 25,000 |

| Advertisement Suspense A/c | 800 | ||

| 1,26,800 | 1,26,800 |

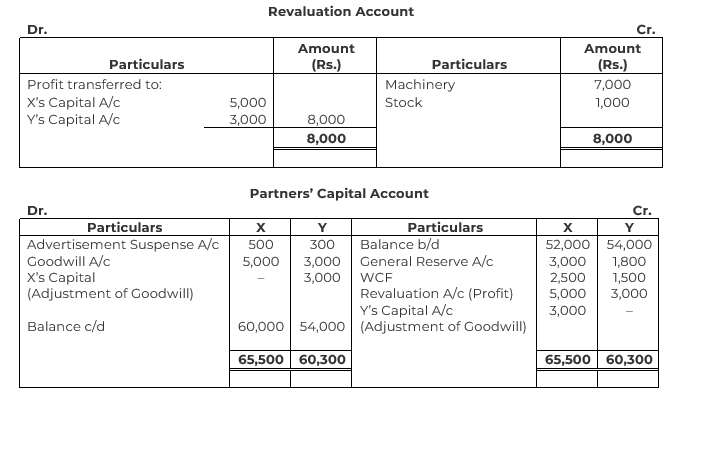

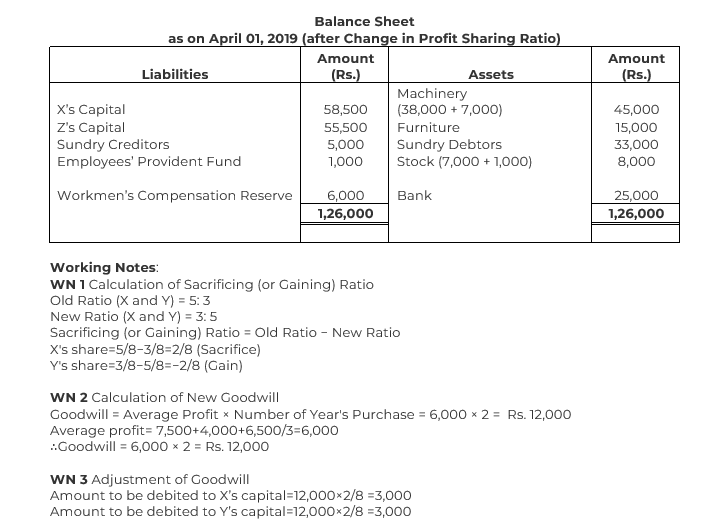

On the above date, they decided to change their profit-sharing ratio to 3 : 5 and agreed upon the following:

(a) Goodwill be valued on the basis of two years’ purchase of the average profit of the last three years. Profits for the years ended 31st March, are: 2016-17 − Rs. 7,500; 2017-18 − Rs. 4,000; 2018-19 − Rs. 6,500.

(b) Machinery and Stock be revalued at Rs. 45,000 and Rs. 8,000 respectively.

(c) Claim on account of workmen compensation is Rs. 6,000.

Prepare Revaluation Account, Partners’ Capital Accounts and the Balance Sheet of the new firm.

Solution