| Liabilities | Amount (Rs.) | Assets | Amount (Rs.) |

| X’s Capital – 10,000 | Cash in Hand | 9,000 | |

| Y’s Capital – 8,000 | 18,000 | Debtors | 11,000 |

| Creditors | 12,000 | Stock | 12,000 |

| General Reserve | 16,000 | Building | 8,000 |

| Workmen Compensation Reserve | 4,000 | Machinery | 10,000 |

| 50,000 | 50,000 |

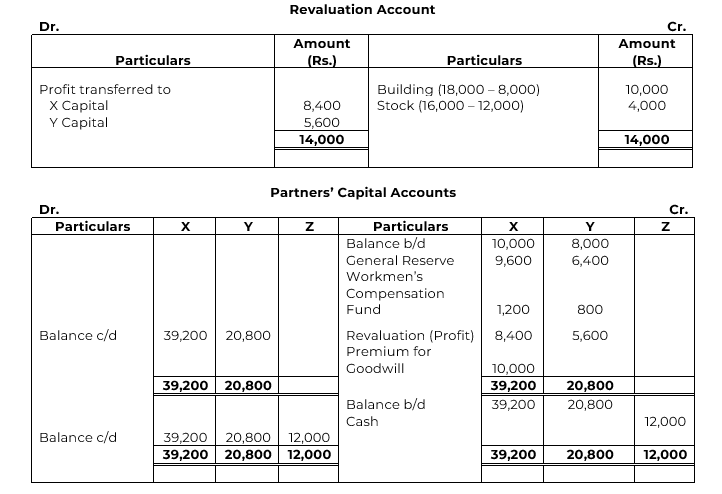

X and Y share profits in the proportion of 3 : 2. The following terms of admission are agreed upon:

(a) Revaluation of assets: Building Rs. 18,000; Stock Rs. 16,000.

(b) The liability on Workmen Compensation Reserve is determined at Rs. 2,000.

(c) Z brought in as his share of goodwill Rs. 10,000 in cash.

(d) Z was to bring in further cash as would make his capital equal to 20% of the combined capital of X and Y after above revaluation and adjustments are carried out.

(e) The further profit-sharing proportions were: X−2/5th, Y−2/5th and Z−1/5th.

Prepare new Balance Sheet of the firm and Capital Accounts of the Partners.

SOLUTION