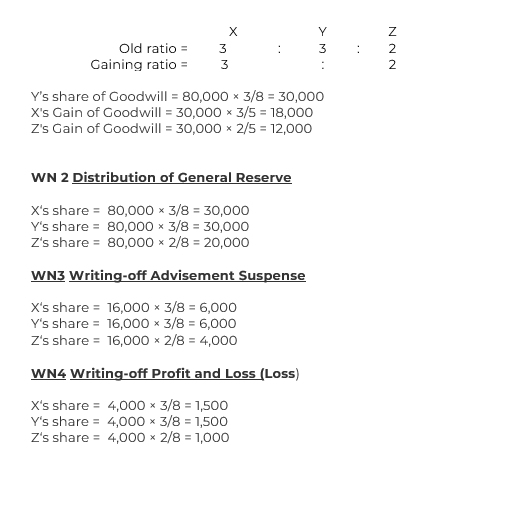

| Liabilities | Amount ( Rs.) | Assets | Amount ( Rs.) |

| Sundry Creditors | 2,50,000 | Cash at Bank | 50,000 |

| General Reserve | 80,000 | Bills Receivable | 60,000 |

| Partners’ Loan A/c : | Debtors – 80,000 | ||

| X – 50,000 | Less: Provision for Doubtful Debts – (4,000) | 76,000 | |

| Y – 40,000 | 90000 | Stock | 1,24,000 |

| Capital A/c : | Fixed Assets | 3,00,000 | |

| X | 1,00,000 | Advertisement Suspense A/c | 16,000 |

| Y | 60,000 | Profit and Loss A/c | 4,000 |

| Z | 50,000 | 2,10,000 | |

| 6,30,000 | 6,30,000 |

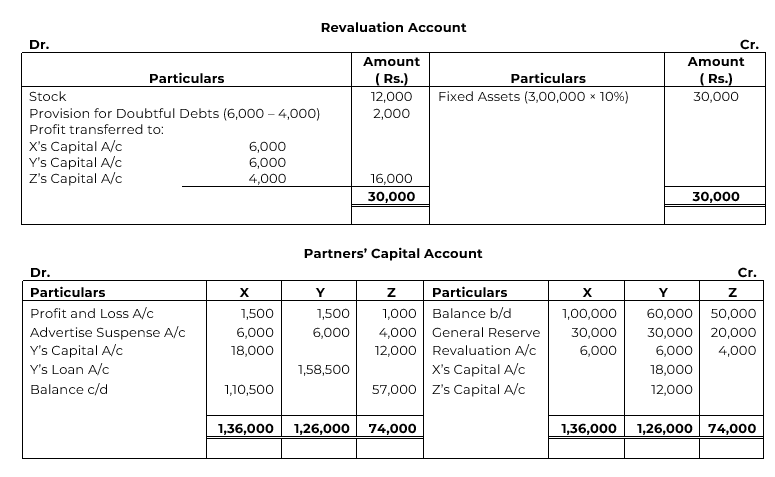

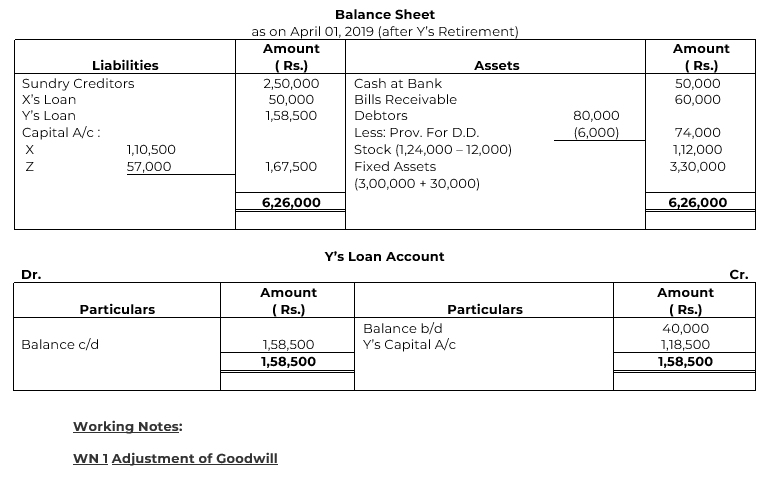

On 1st April, 2019, Y decided to retire from the firm on the following terms:

(a) Stock to be reduced by Rs. 12,000.

(b) Advertisement Suspense Account to be written off.

(c) Provision for Doubtful Debts to be increased to Rs. 6,000.

(d) Fixed Assets be appreciated by 10%.

(e) Goodwill of the firm, valued at Rs. 80,000 and the amount due to the retiring partners be adjusted in X’s and Z’s Capital Accounts.

Prepare Revaluation Account, Partners’ Capital Accounts and the Balance Sheet to give effect to the above

SOLUTION