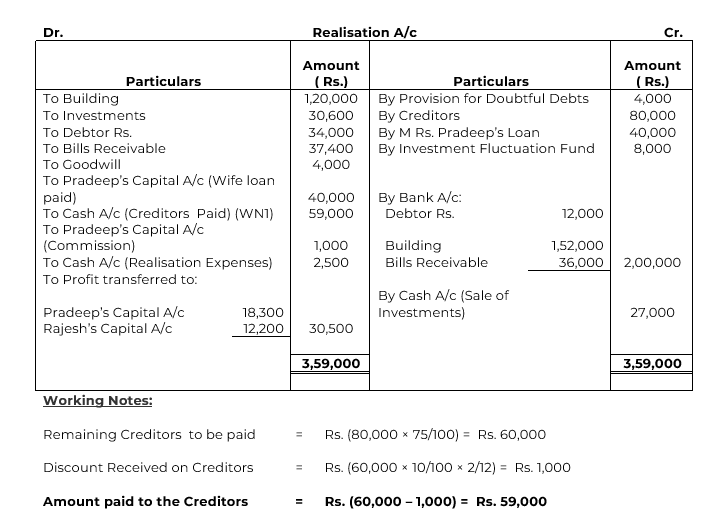

BALANCE SHEET as at 31st March, 2018

| Liabilities | Amount ( Rs.) | Assets | Amount ( Rs.) |

| Creditors | 80,000 | Building | 1,20,000 |

| M Rs. Pradeep’s Loan | 40,000 | Investment | 30,600 |

| Rajesh’s Loan | 24,000 | Debtor Rs. 34,000 | |

| Investment Fluctuation Fund | 8,000 | Less: Provision for Doubtful Debts (4,000) | 30,000 |

| Capital A/c : | Bills Receivable | 37,400 | |

| Pradeep 42,000 | Bank | 6,000 | |

| Rajesh 42,000 | 84,000 | Profit and Loss A/c | 8,000 |

| Goodwill | 4,000 | ||

| 2,36,000 | 2,36,000 | ||

Following terms and conditions were agreed upon:

(a) Pradeep agreed to pay off his wife’s loan.

(b) Half of the debtor realised Rs. 12,000 and remaining debtor Rs. were used to pay off 25% of the Creditors .

(c) Investment sold to Rajesh for Rs. 27,000.

(d) Building realised Rs. 1,52,000.

(e) Remaining Creditors were to be paid after two months, they were paid immediately at 10% p.a. discount.

(f) Bill receivables were settled at a loss of Rs. 1,400.

(g) Realisation expenses amounted to Rs. 2,500.

Preared Realisation Account.

Solution