| Liabilities | Amount (Rs.) | Assets | Amount (Rs.) |

| Creditors | 15,000 | Cash at Bank | 5,000 |

| Employees’ Provident Fund | 10,000 | Sundry Debtors – 20,000 | |

| Workmen Compensation Reserve | 5,800 | Less: Provision for Doubtful Debts – (600) | 19,400 |

| Capital A/c : | Stock | 25,000 | |

| X – 70,000 | Fixed Assets | 80,000 | |

| Y – 31,000 | 1,01,000 | Profit and Loss A/c | 2,400 |

| 1,31,800 | 1,31,800 |

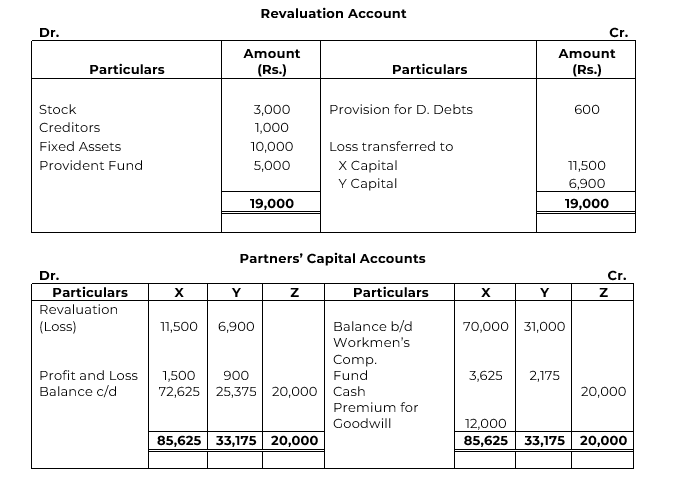

They admit Z into partnership with 1/8th share in profits on 1st April, 2019. Z brings Rs. 20,000 as his capital and Rs. 12,000 for goodwill in cash. Z acquires his share from X. Following revaluations are also made:

(a) Employees’ Provident Fund liability is to be increased by Rs. 5,000.

(b) All Debtors are good.

(c) Stock includes Rs. 3,000 for obsolete items.

(d) Creditors are to be paid Rs. 1,000 more.

(e) Fixed Assets are to be revalued at Rs. 70,000.

Prepare Journal entries, necessary accounts and new Balance Sheet. Also, calculate new profit-sharing ratio.

SOLUTION