| Liabilities | Amount (Rs.) | Assets | Amount (Rs.) |

| Trade Creditors | 1,20,000 | Cash at Bank | 1,80,000 |

| Bills Payable | 80,000 | Stock | 1,40,000 |

| General Reserve | 60,000 | Sundry Debtors | 80,000 |

| Capital A/cs: | Building | 3,00,000 | |

| X – 7,00,000 | Advance to Y | 7,00,000 | |

| Y – 7,00,000 | Profit and Loss A/c | 3,20,000 | |

| Z – 60,000 | 14,60,000 | ||

| 17,20,000 | 17,20,000 |

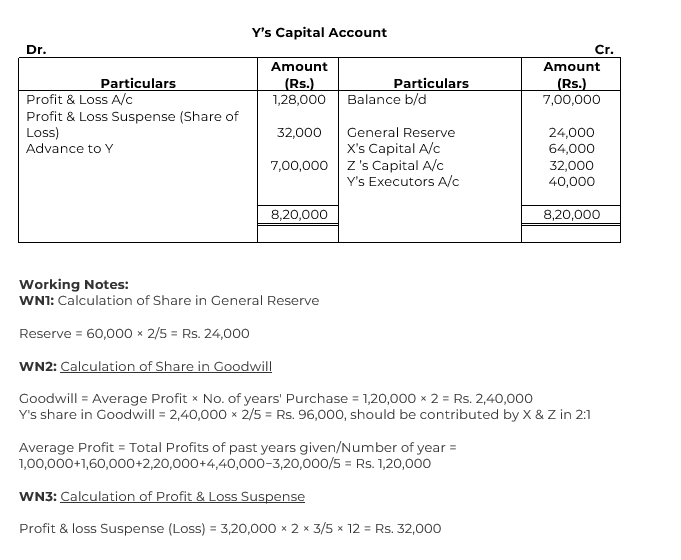

Y died on 30th June, 2020. The Partnership Deed provided for the following on the death of a partner:

(i) Goodwill of the business was to be calculated on the basis of 2 times the average profit of the past 5 years. Profits for the years ended 31st March, 2020, 31st March, 2019, 31st March, 2018, 31st March, 2017 and 31st March, 2016 were Rs. 3,20,000 (Loss); Rs. 1,00,000; Rs. 1,60,000; Rs. 2,20,000 and Rs. 4,40,000 respectively.

(ii) Y’s share of profit or loss from 1st April, 2020 till his death was to be calculated on the basis of the profit or loss for the year ended 31st March, 2020.

You are required to calculate the following:

(a) Goodwill of the firm and Y’s share of goodwill at the time of his death.

(b) Y’s share in the profit or loss of the firm till the date of his death.

(c) Prepare Y’s Capital Account at the time of his death to be presented to his executors.

SOLUTION